The payment method you choose for an Egyptian e-commerce product is not a checkout detail. It is an architectural decision that determines your conversion rate, your operational costs, and how large your addressable market actually is — before you write a single line of business logic.

The Real Cost of the Decision-to-Payment Gap

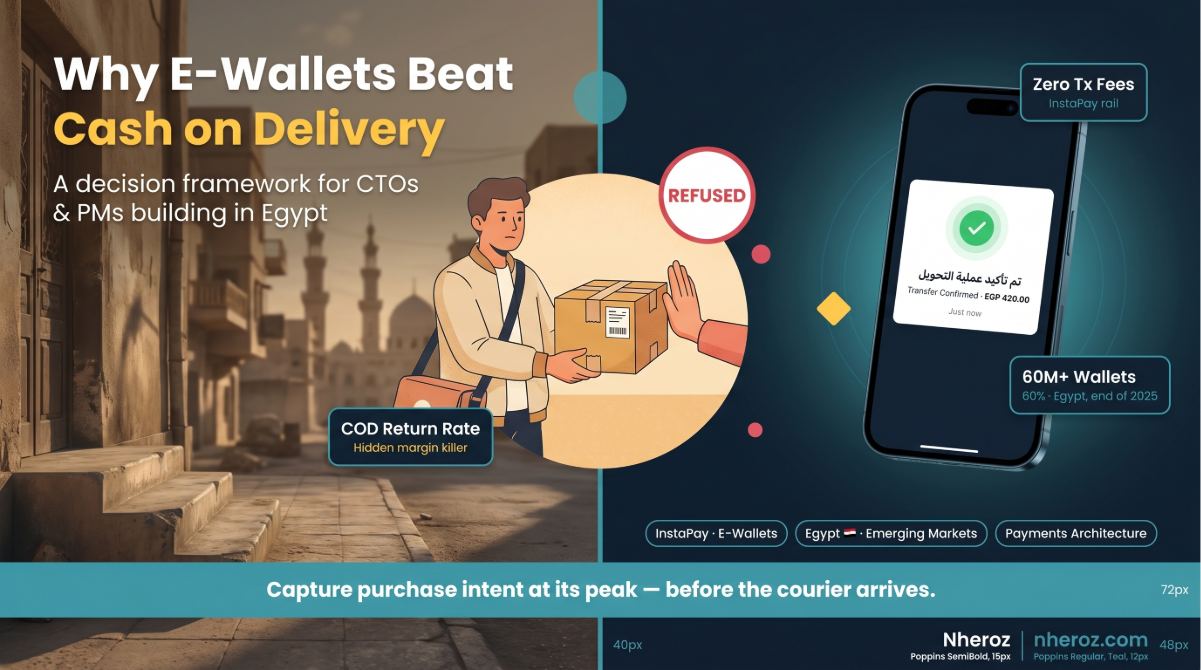

The moment a customer decides to buy is not the moment they decide to pay. In markets with saved cards and one-click checkout, that gap is milliseconds. In cash-on-delivery markets, that gap is days.

A customer adds to cart on Tuesday night. The courier arrives Thursday afternoon. In those 40-plus hours, intent cools — a cheaper option surfaced, payday is still a week away, or the mood simply passed. The result is a refused delivery: the product travels to the customer's door and returns to the warehouse.

Every refused COD order costs you twice: the outbound delivery and the return logistics. The product is locked out of inventory for the full round trip. And none of this appears as a "failed payment" in your dashboard — it surfaces later as a return rate that quietly erodes margin order by order. Your payment method's job is to capture intent at its peak. Any method that separates the decision from the payment by days is structurally leaking revenue.

Why "Just Add Card Payments" Doesn't Solve It

The textbook answer is online card payment: charge at checkout, intent captured, problem solved. The textbook answer assumes your customers have cards.

In Egypt, a significant share of consumers remain unbanked or underbanked. Requiring a Visa or Mastercard at checkout doesn't convert your COD customers into prepaid customers — it filters them out entirely. You've traded a return-rate problem for a smaller market.

Even among customers who do hold cards, a trust barrier persists. Many are reluctant to enter card details on an unfamiliar merchant's website, and for small traders without a recognized brand, "enter your card number here" is a conversion killer in itself. For a CTO, cards also bring real engineering weight: PCI DSS scope, gateway integration and certification, chargeback handling, and settlement cycles that can hold merchant funds for days. That is a substantial infrastructure commitment for a payment rail a meaningful portion of your market cannot use.

Why E-Wallets Are the Right Default for This Market

Mobile wallets and instant payment apps solve both problems simultaneously, and adoption has reached the point where this is no longer a speculative bet. According to Central Bank of Egypt data, mobile wallets in Egypt reached approximately 60 million by end of 2025, up from 15.2 million in 2019, with transaction value hitting roughly EGP 4 trillion. National Telecom Regulatory Authority figures for Q2 2025 showed wallet transaction volume up 80% year-on-year. InstaPay, launched on the CBE's Instant Payment Network in 2022, passed 16 million users by mid-2025, processing over a billion transactions.

Walk through any commercial street in Cairo and you'll observe it directly: a customer who would never share card details transfers money by phone number, daily, without hesitation. The wallet is not a fintech novelty here. It is how a large part of the country already moves money.

Three properties make this decisive for product teams:

- No bank account required. A wallet runs on a phone number and a national ID. Your addressable market expands to include exactly the customers that card-only checkout excludes.

- Payment at the moment of decision. The customer transfers while intent is at its peak, closing the COD gap entirely. No courier carrying cash, no refused delivery, no double logistics cost.

- Pre-existing trust. You are not asking customers to adopt a new behavior or trust your checkout form with sensitive credentials. You are plugging into a payment habit they already perform every day.

The Second-Order Effects Most Teams Miss

Beyond the three core arguments, there are downstream effects that matter specifically to CTOs and PMs making architecture decisions.

Zero or near-zero transaction fees change your pricing model. Card gateways take a percentage of every transaction. Wallet-to-wallet transfers and InstaPay transfers are free or nearly free for amounts typical of small-trader commerce. For merchants operating on thin margins, this is not an optimization — it is the difference between a viable and a non-viable platform fee structure.

Settlement is instant. The merchant sees the money immediately, not in a T+2 batch. For small traders managing daily cash flow, instant settlement is a feature card rails cannot replicate.

Reduced compliance surface. If your platform never touches card data, you never enter PCI DSS scope. Your security investment goes toward protecting what you actually store, not certifying infrastructure for data you would rather not hold.

Chargebacks do not exist on this rail. Wallet transfers are push payments initiated by the customer. There is no chargeback mechanism to misuse, which removes an entire fraud category from your threat model. The trade-off is that refunds become a merchant-initiated process you must design deliberately — but that is a product decision you control, not a liability you inherit.

Resilient to local infrastructure conditions. A wallet transfer works on a low-end Android phone over a weak connection. Card checkout flows with 3D Secure redirects and OTP timeouts frequently do not.

How We Built It in VatrinaView

Building VatrinaView — our multi-tenant e-commerce SaaS platform now serving 50-plus paying merchants in the Egyptian market — we designed the payment layer around InstaPay with document verification. The flow is straightforward: the buyer pays through InstaPay at checkout, uploads a confirmation screenshot, and the seller confirms receipt before the order processes.

Is a manual confirmation step elegant by Silicon Valley standards? No. Is it the right trade-off for this market? Yes — and the reasoning matters. The screenshot-and-confirm flow mirrors exactly how buyers and sellers in this market already transact over WhatsApp and Facebook Marketplace. We did not invent a new trust model; we digitized the one that already works. Both sides see and explicitly approve the transaction, which builds confidence between strangers — the hardest problem in small-merchant e-commerce. And it costs both parties nothing in fees.

Technical decisions are business trade-offs, not purity contests. We accepted a manual verification step in exchange for zero fees, instant settlement, and a trust model the market already understood — the same way we accepted three tiers of image storage in exchange for sub-second load times across variable connections.

The principle generalizes: the best architecture for an emerging market is rarely the one in the Stripe documentation. It is the one that matches how your users already behave.

The Honest Trade-Offs

E-wallet-first does not mean e-wallet-only, and it is not without costs. Build with clear eyes about the following.

- Verification overhead at scale. A screenshot-confirmation flow puts work on the seller. At higher volumes you will want API-based payment verification or webhook integration with wallet providers where available. Design your data model so you can swap the verification mechanism without rebuilding the order flow around it.

- Refunds require explicit product design. Without a chargeback rail, your dispute and refund process is a feature you must build, not a gateway feature you inherit. Design it before you need it, not after your first dispute.

- Fake confirmation risk is real. Screenshots can be edited. Seller confirmation of actual fund receipt — not just document upload — must be the gate that releases the order to fulfillment.

- Cards still belong in your roadmap. If your merchants sell to international customers, or to segments where cards are standard, card support belongs on your backlog as a secondary rail — just not as the default foundation you build everything else around.

A Decision Framework for CTOs and PMs

If you are scoping payments for an Egyptian or structurally similar market, work through this sequence before you commit to an architecture:

- Where is your customer's money? If a significant share of your market is unbanked, card-first checkout shrinks your TAM before you write a line of code.

- How large is your decision-to-payment gap? If you are COD-dependent, measure refused deliveries as a payment problem, not a logistics problem. The fix is upstream.

- What trust model does your market already use? The cheapest trust to build is the trust that already exists. Identify it and plug into it.

- What does each rail cost per transaction — in fees, compliance, and engineering overhead? For small-ticket, thin-margin commerce, the wallet rail typically wins on all three dimensions simultaneously.

The payment layer is where intent converts to revenue, or doesn't. Getting this architecture right early means lower return rates, a larger addressable market, lower per-transaction costs, and a compliance posture you can actually maintain. Start with the rail your users already trust — then layer alternatives as your merchant base grows and demands them.

Nheroz builds custom software for businesses in Egypt, MENA, and beyond. VatrinaView, our multi-tenant SaaS e-commerce platform, currently serves 50-plus paying merchants in the Egyptian market. You can explore a live demo at drmobile.vatrinaview.com.